1. Executive Summary

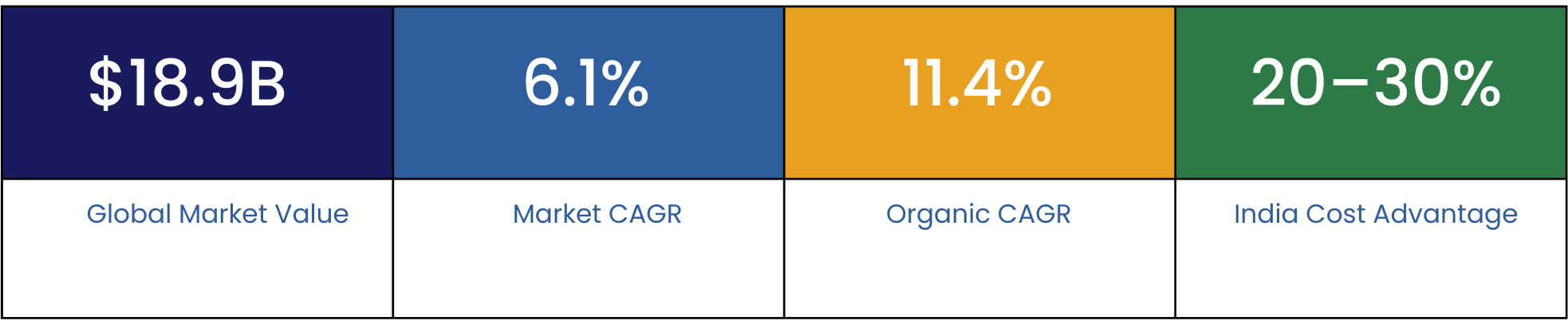

As we progress through 2026, the global frozen french fries market stands at a critical juncture. Currently valued at approximately USD 18.9 Billion, the market is projected to sustain a Compound Annual Growth Rate (CAGR) of 6.1% through the end of the decade. For B2B stakeholders — specifically Importers, Procurement Directors, and Category Managers — the defining narrative of 2025–2026 is supply chain disruption and geographical arbitrage.

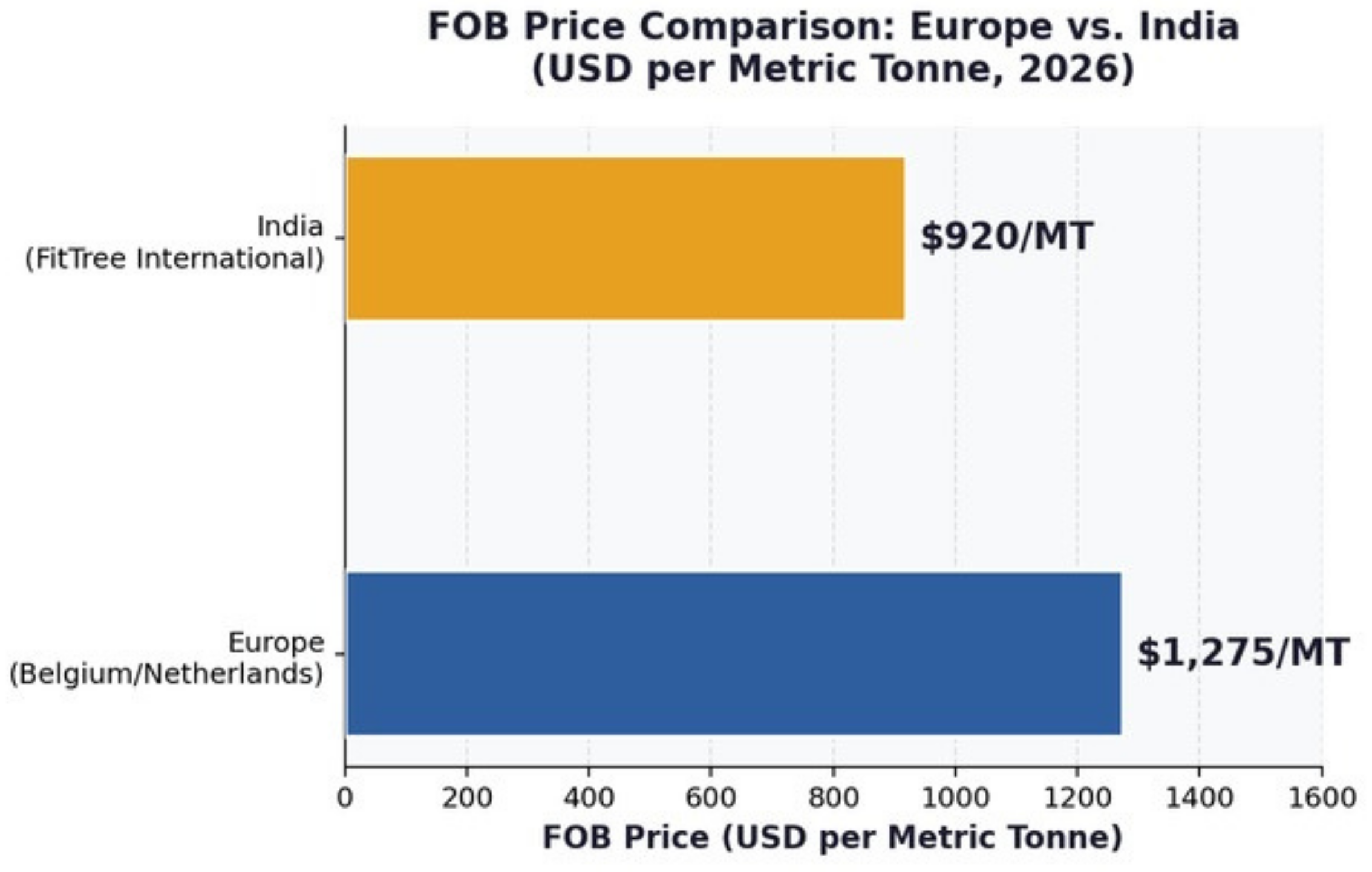

Historically, global procurement departments relied heavily on Western Europe (primarily Belgium and the Netherlands) and North America for frozen potato supplies. That model is now under severe stress. High energy costs, stringent environmental regulations regarding nitrogen emissions, and erratic climate patterns have driven European FOB prices to historic highs of $1,200–$1,350 USD per Metric Tonne.

2. FOB PRICE COMPARISON: EUROPE vs. INDIA

3. WHOLE MARKET DEMAND & GROWTH DYNAMICS

The 6.1% global CAGR is fueled by two distinct drivers across commercial (B2B) and consumer (B2C) channels:

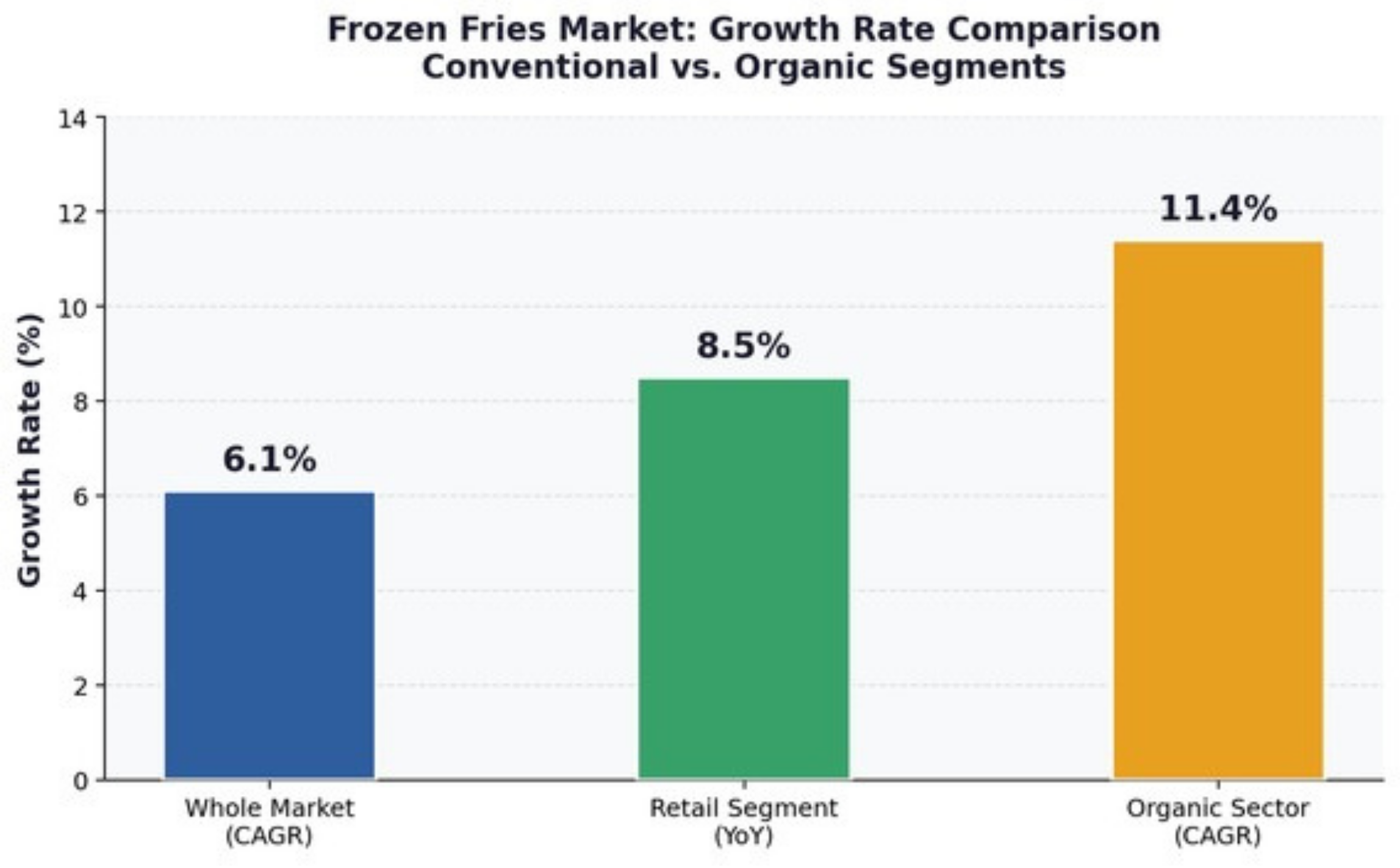

4. THE MARGIN MULTIPLIER: ORGANIC MARKET GROWTH

While standard conventional fries drive volume, Organic Frozen French Fries are driving value and profitability. The organic segment is growing at a remarkable 11.4% CAGR — nearly double the conventional market rate.

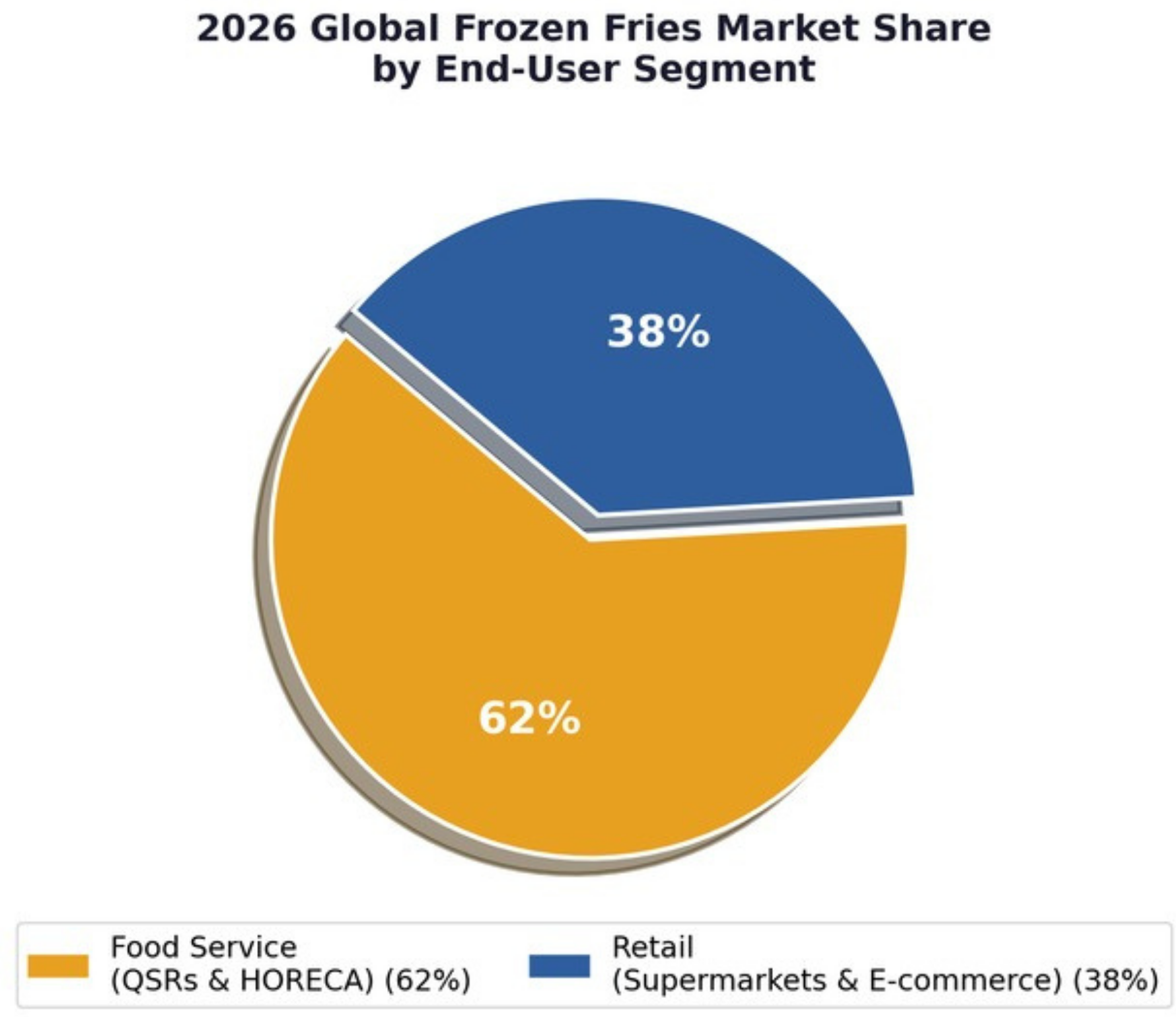

5. MARKET SEGMENTATION: 2026 END-USER ANALYSIS

The following pie chart illustrates the breakdown of global frozen fries consumption by End-User segment in 2026, highlighting where volume and revenue are primarily flowing:

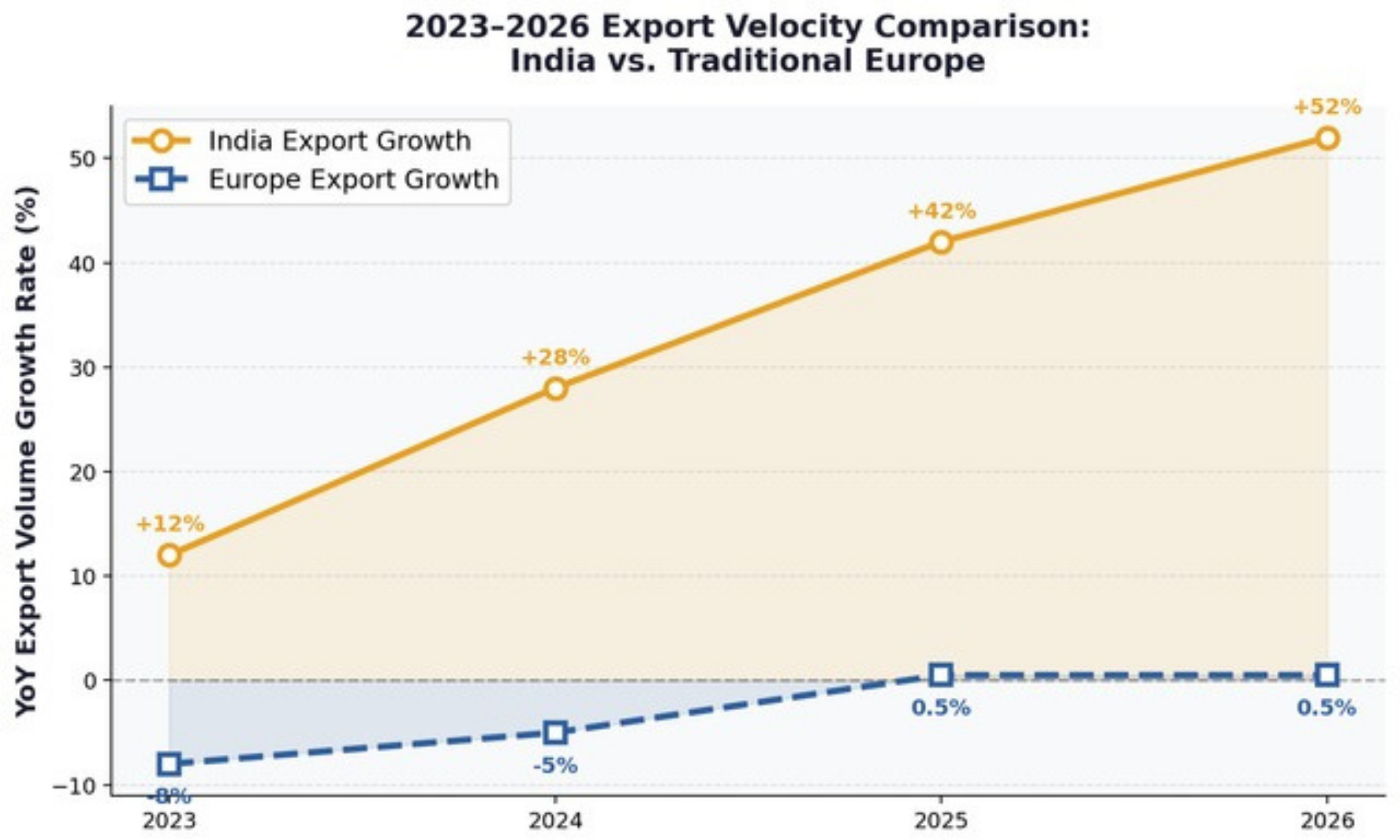

6. GLOBAL EXPORT TRENDS & THE SUPPLY SHIFT

If the pie chart shows who is buying, the export velocity graph shows where buyers are sourcing from. A monumental geographical shift is underway as European supply stagnates while India’s export capacity surges dramatically:

8. CONCLUSION: THE STRATEGIC MANDATE FOR 2026

The 2025–2026 Frozen French Fries market offers immense profitability for the strategic buyer, but severely penalizes those clinging to outdated supply chains. Global demand — buoyed by QSR expansion and at-home consumption — will only continue to rise, and the organic sector presents an unmissable opportunity for margin expansion. To thrive, Importers and Procurement Departments must diversify their geographical risk. Pivoting procurement volumes toward India is no longer an experimental alternative — it is a financial imperative. By partnering with a technologically advanced, vertically integrated supplier like FitTree International LLP, buyers can secure their supply, guarantee international quality standards, and drastically reduce their landed costs.